If you were hurt by a driver who had no insurance, or not enough to cover your injuries, your own uninsured and underinsured motorist coverage is usually what pays. In Missouri, uninsured motorist (UM) coverage applies when the at-fault driver carried no liability insurance or cannot be identified, such as a hit-and-run. Underinsured motorist (UIM) coverage applies when the at-fault driver had some insurance, but their limits were too low to cover what you actually lost. Both are claims you file with your own insurer under your own policy. Empower Injury Law handles these claims for drivers and passengers in Liberty, Clay County, and the north Kansas City metro, and this page explains how the coverage works in Missouri and what to expect.

This is general information about Missouri law, not legal advice about your specific situation. Coverage turns on the exact wording of your policy, and the rules below should be confirmed against your facts before you rely on them.

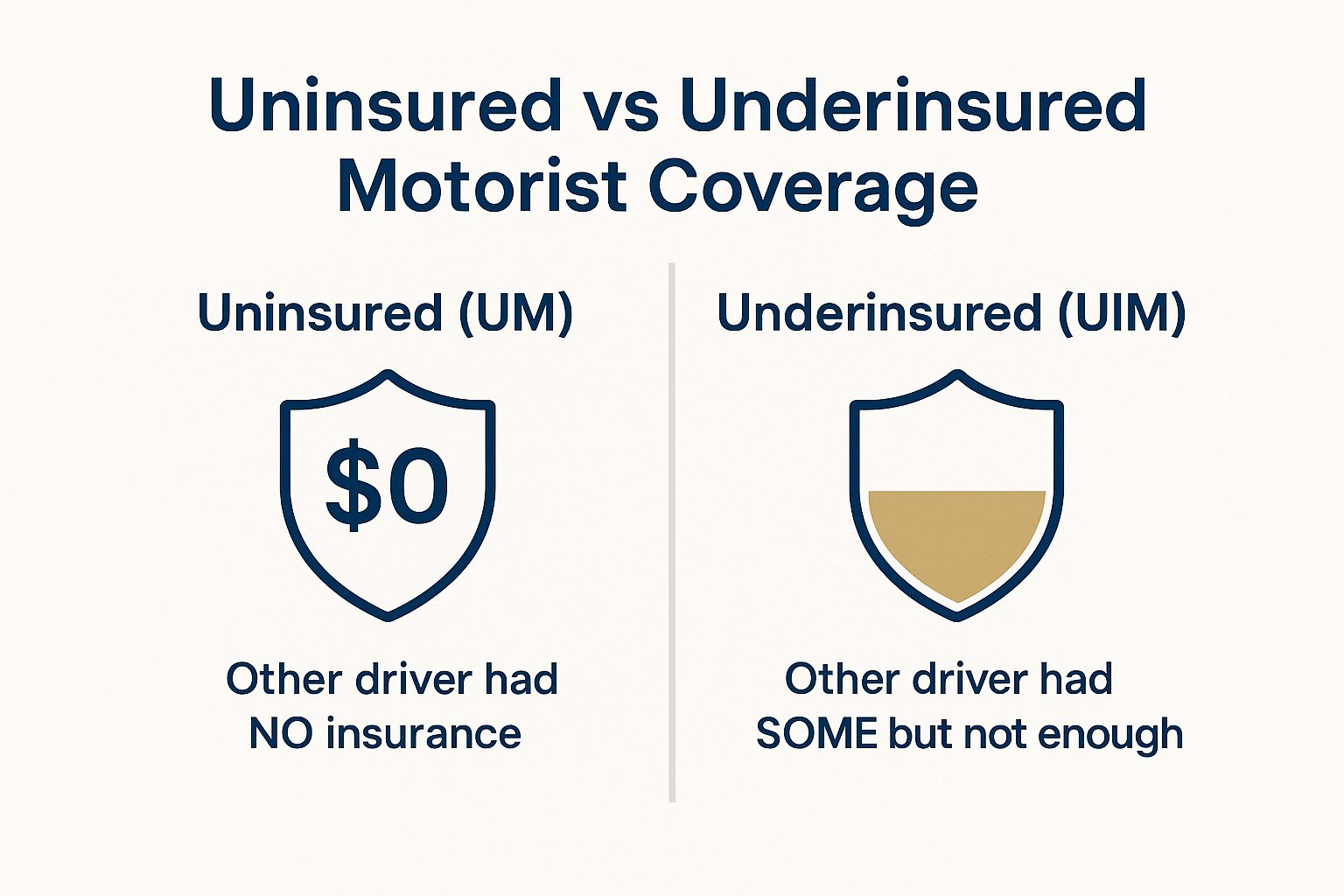

What is uninsured motorist (UM) coverage in Missouri?

Uninsured motorist coverage is part of your own auto policy that pays for your injuries when the at-fault driver had no liability insurance. It stands in for the coverage the other driver was supposed to carry. Because you are collecting from your own insurer rather than the other driver, UM coverage matters most when the at-fault driver has nothing to collect from, which is common.

UM coverage is required on Missouri auto policies, with minimum limits of $25,000 per person and $50,000 per accident for bodily injury under RSMo 379.203. Many drivers carry only those minimum UM limits without realizing it, which becomes a problem when injuries are serious.

UM coverage typically applies in two situations. The first is when the at-fault driver is identified but had no liability insurance at all. The second is a hit-and-run, where the driver who caused the crash fled and cannot be identified. Hit-and-run claims are discussed in more detail below.

What is underinsured motorist (UIM) coverage in Missouri?

Underinsured motorist coverage pays the difference when the at-fault driver had insurance, but not enough. If another driver runs a red light, injures you badly, and carries only a $25,000 liability limit while your medical bills and lost income run well past that, the at-fault policy is exhausted long before your losses are covered. UIM coverage is designed to fill part of that gap, up to your own UIM limits.

UIM coverage works differently from UM coverage in Missouri, and it is treated differently under the law. Underinsured motorist coverage is optional in Missouri. Unlike UM coverage, which every auto policy must include, UIM is coverage you choose to add, so not every driver carries it. Because of that difference, it is worth pulling your own declarations page to see whether you actually carry UIM coverage and at what limit.

UM versus UIM: what is the difference?

The simplest way to keep them straight is to look at what the at-fault driver had:

- Uninsured motorist (UM): the at-fault driver had no liability insurance, or cannot be identified (hit-and-run). Your UM coverage steps in.

- Underinsured motorist (UIM): the at-fault driver had liability insurance, but the limits were too low to cover your losses. Your UIM coverage covers part of the shortfall.

The two coverages answer different questions. UM asks whether there was any coverage on the other side at all. UIM asks whether the coverage on the other side was enough. A single crash can involve both, for example a multi-car wreck where one at-fault driver was uninsured and another was underinsured.

When does each kind of claim apply?

A UM claim generally applies when:

- The at-fault driver had no auto liability insurance at the time of the crash.

- The at-fault driver fled and was never identified (hit-and-run or phantom vehicle).

- The at-fault driver's insurer denied coverage or the policy was not in force.

A UIM claim generally applies when:

- The at-fault driver had liability insurance, but their limits are less than your damages.

- You have settled with or exhausted the at-fault driver's liability policy and still have uncovered losses, and you carry UIM coverage.

Most Missouri policies require you to exhaust the at-fault driver's liability limits before you can collect UIM benefits. Missouri law does not itself impose that requirement; it comes from the policy. Many policies also require you to get your UIM insurer's consent before you settle with the at-fault driver. If you miss one of these policy conditions, Missouri courts have generally required the insurer to show it was actually prejudiced by the misstep before it can deny the claim on that basis, but the safest course is to involve a lawyer before you settle so the conditions are met.

How do you file a UM or UIM claim against your own insurer?

A UM or UIM claim is a first-party claim, meaning you are making a claim under your own contract with your own insurance company. That is different from a liability claim, where you pursue the other driver's insurer. In a first-party claim, your insurer steps into the shoes of the at-fault driver for purposes of paying what that driver should have paid, up to your coverage limits.

In practice, that means you give your insurer prompt notice of the claim, document your injuries and losses, and resolve the value of the claim with your own carrier through negotiation, and if your policy provides for it, through arbitration or a lawsuit. Your policy sets out the specific conditions, including the notice and consent-to-settle requirements discussed above.

A point worth understanding up front: in a UM or UIM claim, your own insurer is on the other side of the dispute over how much your claim is worth. They are not adverse to you the way the other driver's insurer is, but they do have a financial interest in valuing your claim conservatively. That is normal, and it is the reason people often want a lawyer involved even when the claim is against their own carrier.

If your insurer handles a clear UM or UIM claim unreasonably, that can raise separate questions about insurance bad faith. Those questions are governed by their own Missouri rules and are covered separately.

Can you stack UM or UIM coverage in Missouri?

Stacking means adding together the limits of more than one UM or UIM coverage so that more money is available for a single claim. For example, if you have two or three vehicles on one policy, each with its own UM limit, stacking would let you combine those limits. Insurers often write anti-stacking language into their policies to prevent this.

Whether you can stack coverage in Missouri depends on the specific language of your policy, and it is a heavily litigated and still-evolving area of Missouri law. Some policy language allows combining limits across multiple vehicles or policies; other language restricts it through anti-stacking clauses, and whether a particular clause holds up has been the subject of extensive case law. Because the answer turns on the exact wording, reviewing the actual policy is essential.

Because stacking can change the amount of coverage available, sometimes substantially, it is one of the first things to review when injuries are serious and the available limits look too low. It depends on the policy language and the number of vehicles and policies involved.

How does offset or setoff work with UIM coverage?

Offset, sometimes called setoff, is the question of whether your UIM limit is reduced by what you already received from the at-fault driver's insurance. In Missouri this turns heavily on your policy language, and policies handle it in different ways. Under an excess approach, your UIM coverage sits on top of the at-fault driver's limits and adds to them. Under an offset or reduced-by approach, the at-fault payment is subtracted from your UIM limit, so the amount actually available is smaller. Some policies instead pay pro rata alongside other applicable coverage.

Missouri law adds one important protection. Where UIM limits are below $50,000, the coverage is treated as excess, and therefore stackable, so that a driver who carries only minimum coverage is not left paying for protection that turns out to be illusory. Above that level, how offset works comes back to the wording of your specific policy.

This single issue often decides how much a UIM claim is really worth, so it is worth reading the policy carefully and getting it confirmed before assuming what is available.

Is UM or UIM coverage required in Missouri?

UM coverage is required on Missouri auto policies, with minimum limits of $25,000 per person and $50,000 per accident for bodily injury under RSMo 379.203. UIM coverage is a separate question: it is optional in Missouri, so you carry it only if you added it to your policy. Two related points are worth knowing. Missouri has no personal injury protection (PIP) or no-fault system, and medical payments (med pay) coverage is optional. And Missouri's minimum liability limits are $25,000 per person and $50,000 per accident for bodily injury, plus $25,000 for property damage.

The practical takeaway does not depend on the fine print: pull your declarations page and confirm what you carry. People are frequently surprised to learn they declined or never added UIM coverage, or that they carry only minimum UM limits. The general consumer guidance from the Missouri Department of Commerce and Insurance is a reasonable starting point for understanding what coverage you are required to carry and what is optional.

How is a UM or UIM claim's value assessed?

The value of a UM or UIM claim depends on the same things that drive any injury claim: the nature and severity of your injuries, your medical treatment and bills, lost income, the effect on your daily life, and how clearly fault and damages can be shown. There is no formula and no guaranteed result. Every claim is different, and the available coverage limits cap what can be recovered regardless of how serious the injuries are.

Missouri follows pure comparative fault, the rule its courts adopted in Gustafson v. Benda to replace the older contributory-negligence approach. Your recovery is reduced by your own percentage of fault, but you are not barred from recovering even if you were partly at fault. If you were found 20 percent at fault, for example, your recoverable damages would be reduced by that 20 percent. Pure comparative fault means there is no cutoff that wipes out your claim simply because your share of fault crossed a threshold, which is how some other states handle it. This same rule applies in a UM or UIM claim, because your insurer stands in for the at-fault driver.

We do not promise outcomes, and no honest lawyer can. What we can do is evaluate the coverage available, the strength of the liability and damages picture, and the realistic range a claim like yours tends to fall into.

What are the time limits for a UM or UIM claim in Missouri?

For most Missouri personal injury claims, the statute of limitations is five years from the date of injury under RSMo 516.120. That five-year period applies to the underlying negligence claim against an at-fault driver.

A UM or UIM claim runs on a different clock, because it is a claim under your insurance contract rather than a tort claim against the other driver. In Missouri, a claim on a written contract, including a UM or UIM claim against your own insurer, generally has a 10-year limitations period under RSMo 516.110, which is longer than the 5-year period for the underlying injury claim. (A separate vexatious-refusal claim against an insurer runs on the shorter 5-year clock.)

Separate from the lawsuit deadline, most policies require you to notify your insurer of a UM or UIM claim promptly. Missouri law does not set a fixed notice deadline; the requirement comes from your policy, and whether a late notice can actually defeat a claim depends on the circumstances, including whether the insurer was prejudiced by the delay. Because the timing rules overlap, the safe practice is to treat a UM or UIM claim as time-sensitive and put your insurer on notice early.

How an uninsured driver crash typically unfolds in the Northland

Crashes that turn into UM or UIM claims happen on the same Clay County roads as any other wreck. The interchange of Interstate 35 and Missouri Route 152, the I-35 corridor through Liberty and Gladstone, Route 291, and the surface streets feeding off them all see their share of serious collisions. When the at-fault driver in one of those crashes turns out to be uninsured, or flees the scene, the injured driver's own coverage becomes the question.

For drivers in Liberty, Kearney, Gladstone, and North Kansas City, that means the claim is often handled close to home: a Clay County resident, a Missouri policy, and Missouri law. A civil suit arising from one of these crashes would generally be filed in the Circuit Court of Clay County. Knowing the local landscape, the courts, and the carriers that write a lot of policies in the Northland is part of handling these claims well.

If your crash was a more general car accident question rather than a coverage question, our Liberty car accident lawyer page and our Kansas City car accident lawyer page cover the broader process. UM and UIM coverage applies no matter what you were driving, so the same coverage questions come up whether you were in a car, a truck, or on a motorcycle when an uninsured or underinsured driver hit you. For the broader picture of how the firm handles injury claims across the Northland, see our Liberty personal injury lawyer page.

How Empower Injury Law helps with UM and UIM claims

UM and UIM claims sound simple, your own insurer pays, but in practice they turn on coverage details that are easy to get wrong: which coverage applies, whether limits can be stacked, whether an offset reduces what is available, and what deadlines control. We handle these claims for injured drivers and passengers in Liberty and across the Northland, and the work usually involves:

- Reading your policy and declarations page to confirm what UM and UIM coverage you actually have, and at what limits.

- Identifying every applicable policy and coverage, including whether stacking may increase what is available.

- Documenting the injuries, treatment, and losses that drive the claim's value.

- Dealing with your insurer's adjusters and their requests, including recorded-statement requests, so you are not navigating that alone.

- Watching the deadlines, both the lawsuit clock and any policy notice or suit-limitation provisions.

We work on a contingency fee, which means there is no fee unless there is a recovery, and the initial consultation is free.

Frequently asked questions

Does my own insurance pay if an uninsured driver hits me in Missouri?

Usually, yes, through your uninsured motorist (UM) coverage. UM coverage is part of your own auto policy and is designed to pay for your injuries when the at-fault driver had no liability insurance or cannot be identified. You file the claim with your own insurer rather than chasing the uninsured driver directly.

What is the difference between uninsured and underinsured motorist coverage?

Uninsured motorist (UM) coverage applies when the at-fault driver had no insurance or cannot be identified, such as a hit-and-run. Underinsured motorist (UIM) coverage applies when the at-fault driver had insurance, but the limits were too low to cover your losses. UM is about whether there was any coverage; UIM is about whether the coverage was enough.

Is uninsured motorist coverage required in Missouri?

Uninsured motorist coverage is required on Missouri auto policies, with minimum limits of $25,000 per person and $50,000 per accident for bodily injury under RSMo 379.203. Underinsured motorist coverage is optional. Missouri also has no PIP or no-fault system, and medical payments coverage is optional. Check your declarations page to see exactly what you carry.

Can I stack uninsured or underinsured motorist coverage in Missouri?

Stacking means combining the limits of more than one UM or UIM coverage to increase the money available for one claim. Whether you can stack depends on your policy language and the number of vehicles and policies involved, and insurers often include anti-stacking clauses. It is a heavily litigated area of Missouri law, so reviewing your specific policy is the only reliable way to know what is available.

How long do I have to file an uninsured or underinsured motorist claim in Missouri?

Most Missouri personal injury claims must be filed within five years of the injury under RSMo 516.120. A UM or UIM claim is a contract claim against your own insurer, and in Missouri it generally has a longer 10-year limitations period under RSMo 516.110. Most policies also require prompt notice, so treat these claims as time-sensitive and notify your insurer early.

Do I have to give my insurer a recorded statement for a UM claim?

Your insurer may ask for a recorded statement as part of a UM claim, and policies often include a duty to cooperate. That does not mean you have to handle the request alone or unprepared. It is reasonable to speak with a lawyer before giving a recorded statement so you understand what is being asked and why.

Will filing a UM or UIM claim raise my rates?

This depends on your insurer and the circumstances, and it is not something a law firm can promise either way. A UM or UIM claim is a claim against coverage you paid for, for a loss someone else caused. If rate impact is a concern, it is a fair question to raise with your insurer or agent.

Talk with a Liberty UM/UIM lawyer

If an uninsured or underinsured driver injured you in Liberty or the surrounding Northland, you can talk through your options with Empower Injury Law at no cost. We will look at your policy, explain which coverage applies, and tell you honestly what we think the claim involves. There is no pressure and no fee unless there is a recovery.

Call the Liberty office at 816-367-6937, or request a free case review through the form on this page. We serve clients in Liberty, Clay County, Kearney, Gladstone, North Kansas City, and the surrounding Missouri communities.