Hit by an Uninsured Driver in Missouri: What to Do and Who Pays

If an uninsured driver hit you in Missouri, your own uninsured motorist (UM) coverage is usually what pays for your injuries. UM coverage is part of your own auto policy, and it is designed for exactly this situation: the at-fault driver had no liability insurance, or fled the scene and cannot be identified. You file the claim with your own insurer rather than trying to collect from a driver who has nothing to collect from. This article walks through what to do right after the crash, who actually pays, and the mistakes that can quietly hurt your claim. Empower Injury Law handles these claims for drivers and passengers in Liberty and the north Kansas City metro.

This is general information about Missouri law, not legal advice about your specific situation. What applies to your claim depends on your policy and your facts.

What to do right after a crash with an uninsured driver

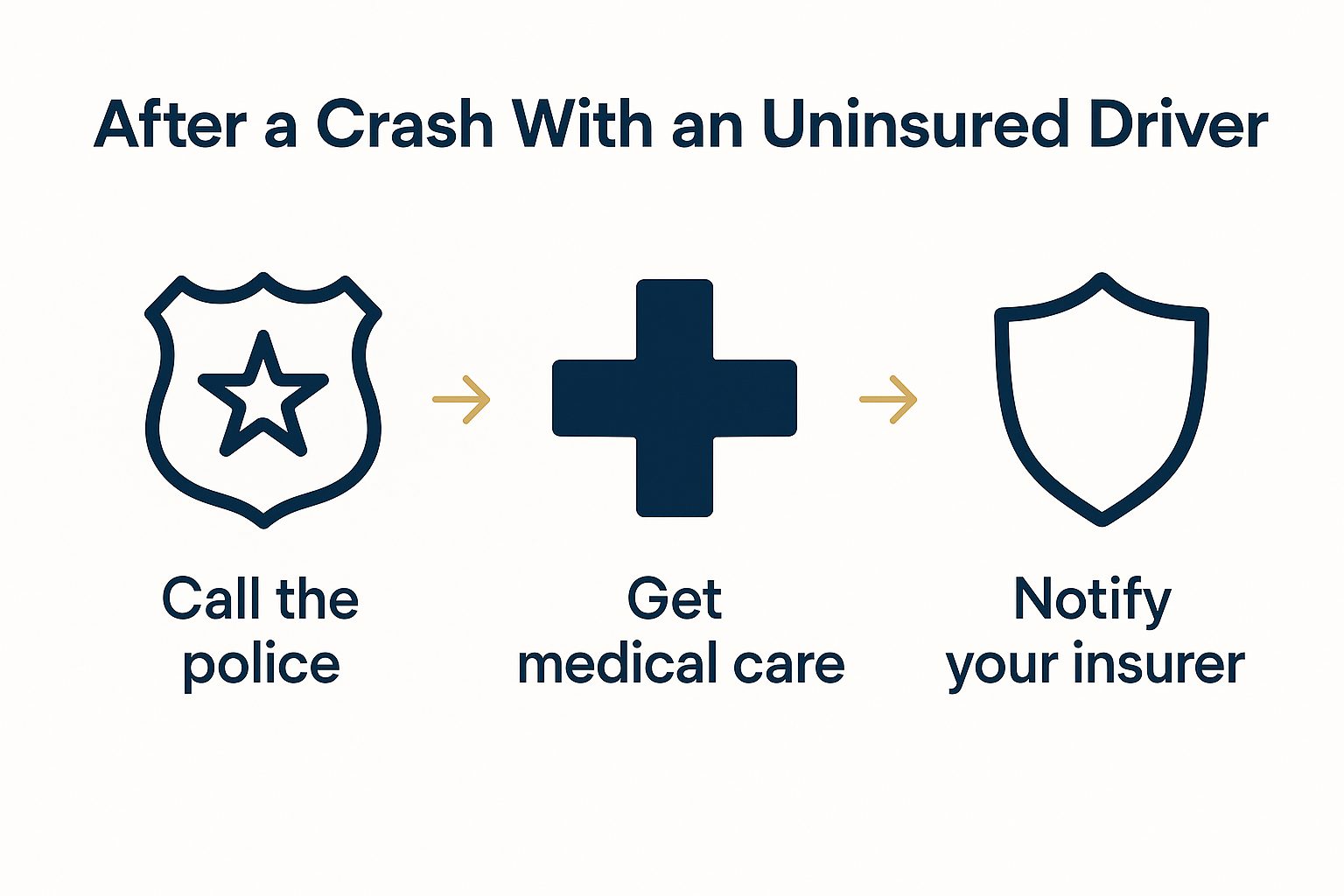

The steps after a crash with an uninsured driver are mostly the same as any crash, with a few that matter more because the other driver may have nothing and may try to leave.

- Get to safety and check for injuries. If anyone is hurt, call 911. Federal crash guidance from NHTSA is straightforward here: move out of traffic if you safely can, and get medical help first.

- Call the police and let them document the scene. A police report is often the only neutral record of what happened, and it is especially useful when the other driver has no insurance or leaves.

- Get the other driver's information if you can, including name, license, plate, and any insurance card, even one that turns out to be expired or invalid.

- Take photos of the vehicles, the scene, the road, and your visible injuries. Get names and numbers of any witnesses.

- Do not let the other driver talk you out of calling the police or into a private "cash" arrangement at the scene. That is a common move from someone who knows they are uninsured.

- See a doctor, even if you feel okay at first. Some injuries surface a day or two later, and a gap in treatment can become an issue later in the claim.

Once you are safe and treated, notify your own insurer that you were in a crash and that the other driver appears to be uninsured. Missouri law does not set a fixed deadline for this, but your policy will require prompt notice, so do it as soon as you reasonably can.

Who pays when the at-fault driver has no insurance?

When the at-fault driver has no liability insurance, your uninsured motorist (UM) coverage is the source that pays. Because there is no other-driver policy to pursue, this is a claim against your own insurer under your own policy. Your insurer effectively steps into the shoes of the driver who should have been insured, and pays for your injuries up to your UM limits.

Two practical points are worth knowing. First, you cannot get more than your UM limits, so the amount of UM coverage you carry matters a great deal. Many Missouri drivers carry only minimum UM limits without realizing it. Second, the uninsured driver is usually not a realistic source of money. You can sometimes still pursue them directly, but a driver who could not afford insurance often cannot pay a judgment either, which is the whole reason UM coverage exists.

Missouri sees a meaningful share of uninsured drivers on the road, which is part of why this coverage matters. The Insurance Information Institute publishes national and state-level data on uninsured driver rates, and the figures are high enough that UM claims are common rather than rare.

For the full picture of how UM and UIM coverage work in Missouri, including stacking, offsets, and deadlines, see our main guide on uninsured and underinsured motorist claims.

What if it was a hit-and-run?

A hit-and-run, where the driver who caused the crash flees and is never identified, is treated as an uninsured motorist situation in Missouri. There is no other driver to identify and no liability policy to pursue, so your own UM coverage is again the source that pays. Missouri does not require physical contact with the phantom vehicle, or independent corroboration, for this kind of UM claim, though reporting the crash promptly still helps.

Two things help a hit-and-run claim. Report it to the police promptly and get a report number, and notify your insurer quickly. A police report is not legally required to pursue a UM claim in Missouri, but reporting matters here even more than usual, because the insurer cannot verify the crash against another driver's account.

What not to do after an uninsured-driver crash

A few avoidable mistakes come up again and again:

- Do not give a recorded statement to any insurer under pressure before you understand what is being asked. Your own insurer may ask for one as part of a UM claim, and your policy may include a duty to cooperate, but you can prepare or speak with a lawyer first. Adjusters take recorded statements early for a reason, and an offhand comment can be used to minimize the claim later.

- Do not accept a fast, low settlement before you know the full extent of your injuries. Some injuries take time to show, and once you settle, you generally cannot reopen the claim.

- Do not skip or delay medical treatment. Gaps in treatment are routinely used to argue that an injury was not serious or was not caused by the crash.

- Do not assume you have no options just because the other driver was uninsured. The whole point of UM coverage is that you usually do.

If you want the broader process for a Missouri crash, our Liberty car accident lawyer page and our Kansas City car accident lawyer page cover what to expect from start to finish.

How Empower Injury Law can help

If an uninsured or hit-and-run driver hurt you in Liberty or the surrounding Northland, you can talk it through with us at no cost. We will look at your own policy to confirm your UM coverage and limits, deal with the adjuster and any recorded-statement request, and watch the deadlines so a notice or reporting requirement does not quietly cut off the claim. We work on a contingency fee, so there is no fee unless there is a recovery.

Call the Liberty office at 816-367-6937, or request a free case review through the form on this page.

Frequently asked questions

Who pays if an uninsured driver hits me in Missouri?

Usually your own uninsured motorist (UM) coverage pays. Because the at-fault driver had no liability insurance, you file the claim with your own insurer under your own policy, up to your UM limits, rather than trying to collect from a driver who has no coverage.

Is a hit-and-run covered by uninsured motorist coverage in Missouri?

Yes. When the driver who caused the crash flees and cannot be identified, there is no liability policy to pursue, so the claim is handled under your own uninsured motorist coverage. Some policies include specific conditions for an unidentified "phantom vehicle" claim, so it is worth confirming the details with a lawyer.

Do I need a police report to make an uninsured motorist claim?

A police report is not legally required to pursue a UM claim in Missouri, but it is strongly recommended and is often the best neutral record of the crash, especially when the other driver is uninsured or fled.

How soon do I have to tell my insurer about an uninsured-driver crash?

Notify your insurer as soon as you reasonably can. Missouri law does not set a fixed deadline, but most policies require prompt notice, and a delay can become an issue, so treat the claim as time-sensitive.

Should I give the insurance company a recorded statement?

You are not required to give a rushed recorded statement before you understand the request. Your own insurer may ask for one as part of a UM claim, and your policy may include a duty to cooperate, but it is reasonable to prepare or talk to a lawyer first so an early comment is not used to minimize your claim.

Author Bio

Kevin A. Jones | Personal Injury Lawyer

Kevin A. Jones, founder and managing attorney of Empower Injury Law, has been practicing law since 2009. With over $25 million in jury verdicts and settlements in his first decade, Kevin has earned a reputation as a fierce advocate for his clients.

Kevin’s approach to law is rooted in his passion for helping people who have been mistreated by corporations, insurance companies, and other powerful entities.

Whether representing individuals wronged by negligent drivers or those injured on someone else’s property, Kevin is dedicated to achieving justice. His extensive experience in the courtroom ensures that clients receive strong, personalized representation that delivers results.