If an uninsured or underinsured driver hurt you in Lawrence or anywhere in Douglas County, uninsured motorist coverage on your own Kansas auto policy is usually what pays. Uninsured motorist (UM) coverage applies when the at-fault driver carried no liability insurance or cannot be identified, such as a hit-and-run. Underinsured motorist (UIM) coverage applies when the driver had some insurance, but not enough to cover what you actually lost. Both are first-party claims, meaning you file them with your own insurer under your own policy. Empower Injury Law handles these claims for drivers and passengers in Lawrence, the KU area, and across Douglas County, and this page explains how the coverage works under Kansas law and what to expect.

This is general information about Kansas law, not legal advice about your specific situation. Coverage turns on the exact wording of your policy and the facts of your crash, so the points below should be confirmed against your circumstances before you rely on them.

On this page

- What is uninsured motorist (UM) coverage in Kansas?

- What is underinsured motorist (UIM) coverage in Kansas?

- UM vs UIM: what is the difference?

- Is UM/UIM coverage required in Kansas?

- How does UM/UIM interact with Kansas PIP (no-fault)?

- Can you stack UM/UIM coverage in Kansas?

- How does a hit-and-run or phantom vehicle work?

- How do you file a UM or UIM claim against your own insurer?

- What are the deadlines for a Kansas UM/UIM claim?

- How UM/UIM claims play out around Lawrence and Douglas County

- How Empower Injury Law helps

- Frequently asked questions

What is uninsured motorist (UM) coverage in Kansas?

Uninsured motorist coverage is the part of your own Kansas auto policy that pays for your bodily injuries when the at-fault driver had no liability insurance. It stands in for the coverage the other driver was supposed to carry but did not. Because you collect from your own insurer rather than from an empty pocket, UM coverage matters most exactly when the at-fault driver has nothing worth pursuing, which is common.

UM coverage is required on Kansas auto policies. The mechanics are set out in K.S.A. 40-284, the Kansas uninsured and underinsured motorist statute. Under that statute, uninsured motorist protection is written into every qualifying Kansas policy, and it cannot simply be left out. The required minimum limits track the state's minimum bodily-injury liability limits, commonly stated as $25,000 per person and $50,000 per accident.

UM coverage typically applies in two situations. The first is when the at-fault driver is identified but carried no liability insurance at all. The second is a hit-and-run, where the driver who caused the crash fled and cannot be identified. Hit-and-run situations are covered in more detail below.

What is underinsured motorist (UIM) coverage in Kansas?

Underinsured motorist coverage pays part of the difference when the at-fault driver had liability insurance, but not enough to cover your losses. If another driver runs a light at 23rd and Iowa, injures you seriously, and carries only a minimum liability limit while your medical bills and lost income run well past that, the at-fault policy is exhausted long before your losses are. UIM coverage is designed to fill part of that gap, up to your own UIM limits.

In Kansas, UIM coverage is not a separate optional add-on the way it is in some states. Under K.S.A. 40-284, the underinsured motorist provision is built into the uninsured motorist coverage, so a Kansas policy that carries UM coverage generally carries UIM coverage at the same limit. This is a real difference from Missouri, where UIM is optional. It is one of the reasons Kansas and Missouri coverage should never be analyzed the same way.

Kansas compares limits to limits. UIM coverage generally kicks in only where your own UM/UIM limit is higher than the at-fault driver's bodily-injury liability limit, and it pays the amount by which your limit exceeds theirs. A practical consequence is that if you carry only the minimum UM/UIM limit and the at-fault driver carried the same minimum liability limit, there may be no UIM gap to collect, because the limits are equal. That is a strong reason to carry UM/UIM limits above the state minimum, and to pull your declarations page and check what you actually have.

UM vs UIM: what is the difference?

The simplest way to keep them straight is to look at what the at-fault driver had.

- Uninsured motorist (UM): the at-fault driver had no liability insurance, or cannot be identified (a hit-and-run). Your UM coverage steps in.

- Underinsured motorist (UIM): the at-fault driver had liability insurance, but the limits were too low. Your UIM coverage covers part of the shortfall, to the extent your limit exceeds theirs.

The two coverages answer different questions. UM asks whether there was any coverage on the other side at all. UIM asks whether the coverage on the other side was enough. A single crash can involve both, for example a multi-vehicle wreck where one at-fault driver was uninsured and another was underinsured.

Is UM/UIM coverage required in Kansas?

Yes. Kansas requires uninsured motorist coverage on auto policies, and because the underinsured motorist provision is folded into UM coverage under K.S.A. 40-284, UIM coverage generally comes with it. The commonly stated minimum is $25,000 per person and $50,000 per accident for bodily injury. A named insured may reject UM/UIM coverage above the statutory minimum, but that rejection has to be in writing, and it does not eliminate the base coverage the statute requires.

Kansas is also a no-fault state, which is a separate requirement layered on top of UM/UIM. Every qualifying policy must include personal injury protection (PIP) benefits under the Kansas Automobile Injury Reparations Act. How PIP and UIM fit together is explained in the next section.

The practical takeaway does not depend on the fine print. Pull your declarations page and confirm the UM/UIM limit you carry. People are frequently surprised to learn they carry only the state minimum, which in Kansas can leave little or no room for a UIM claim because of the limits-to-limits comparison. The Kansas Insurance Department auto insurance page is a reasonable, neutral starting point for understanding what coverage you must carry and what is optional. The Insurance Information Institute and the National Association of Insurance Commissioners publish general consumer explanations of UM/UIM coverage as well.

How does UM/UIM interact with Kansas PIP (no-fault)?

This is where Kansas differs most sharply from Missouri, and it is the part people get wrong most often. Kansas is a no-fault state under the Kansas Automobile Injury Reparations Act, cited at K.S.A. 40-3101 and following, with the required policy contents set out in K.S.A. 40-3107. Missouri has no PIP or no-fault system at all, so a Missouri analysis simply does not transfer here.

Under Kansas no-fault, your own PIP coverage pays certain economic losses first, regardless of who caused the crash. The minimum PIP benefits are set by K.S.A. 40-3103: medical expenses of at least $4,500; rehabilitation expenses of at least $4,500; disability or lost income benefits of at least $900 per month for up to one year; substitution or essential-services benefits of up to $25 per day for up to 365 days; funeral or burial expenses of up to $2,000; and survivors' benefits of at least $900 per month for up to one year. Your policy may carry higher limits, so check your declarations page. PIP does not pay for pain and suffering or other non-economic loss. To reach non-economic damages against an at-fault driver, Kansas law generally requires you to meet a threshold, which is a distinct feature of the no-fault system.

When an uninsured or underinsured driver caused the crash, PIP and UM/UIM both come into play, and the two are designed to work together without paying you twice for the same loss. Your PIP benefits do not reduce or offset your UM/UIM coverage, so your available coverage limit is not shrunk by what PIP pays. At the same time, your UM/UIM coverage will not pay again for damages PIP has already covered, such as medical bills PIP paid. The result is that PIP and UM/UIM coordinate to make you whole once, with no double recovery for the same loss. The PIP anti-duplication and subrogation mechanics are set out in K.S.A. 40-3113a, and how they apply depends on your policy and the facts of your claim.

Can you stack UM/UIM coverage in Kansas?

Stacking means adding together the limits of more than one UM or UIM coverage so that more money is available for a single claim, for example combining the UM limits on two or three vehicles listed on one policy.

Kansas generally does not allow stacking of UM/UIM coverage. K.S.A. 40-284(d) contains an antistacking provision, and the total UM/UIM limits available for a single claim generally cannot exceed the highest limit of any one applicable policy, no matter how many policies or vehicles are involved. This is another point where Kansas and Missouri diverge. Missouri stacking questions turn heavily on policy language and case law, while Kansas has a statutory antistacking rule. Do not carry a Missouri stacking assumption across the state line.

Because Kansas caps the available coverage this way, the practical focus shifts to identifying the single policy with the highest applicable limit and confirming which coverages apply, rather than trying to combine several.

How does a hit-and-run or phantom vehicle work?

If a driver caused your crash and fled before being identified, your uninsured motorist coverage is generally the coverage that responds, because there is no at-fault insurer to pursue. That includes a classic hit-and-run and, in some cases, a phantom vehicle that ran you off the road without contact. Whether and how coverage applies to an unidentified or no-contact vehicle can depend on your policy terms and on corroboration of what happened.

Two practical steps help protect a hit-and-run claim. Report the crash to law enforcement promptly, so there is a contemporaneous record, and notify your own insurer without delay. Prompt reporting does not guarantee coverage, but a gap or a late report can give the insurer an argument it would not otherwise have.

How do you file a UM or UIM claim against your own insurer?

A UM or UIM claim is a first-party claim, meaning you are making a claim under your own contract with your own insurance company. That is different from a liability claim, where you pursue the other driver's insurer. In a first-party UM/UIM claim, your insurer effectively steps into the shoes of the at-fault driver for purposes of paying what that driver should have paid, up to your coverage limits.

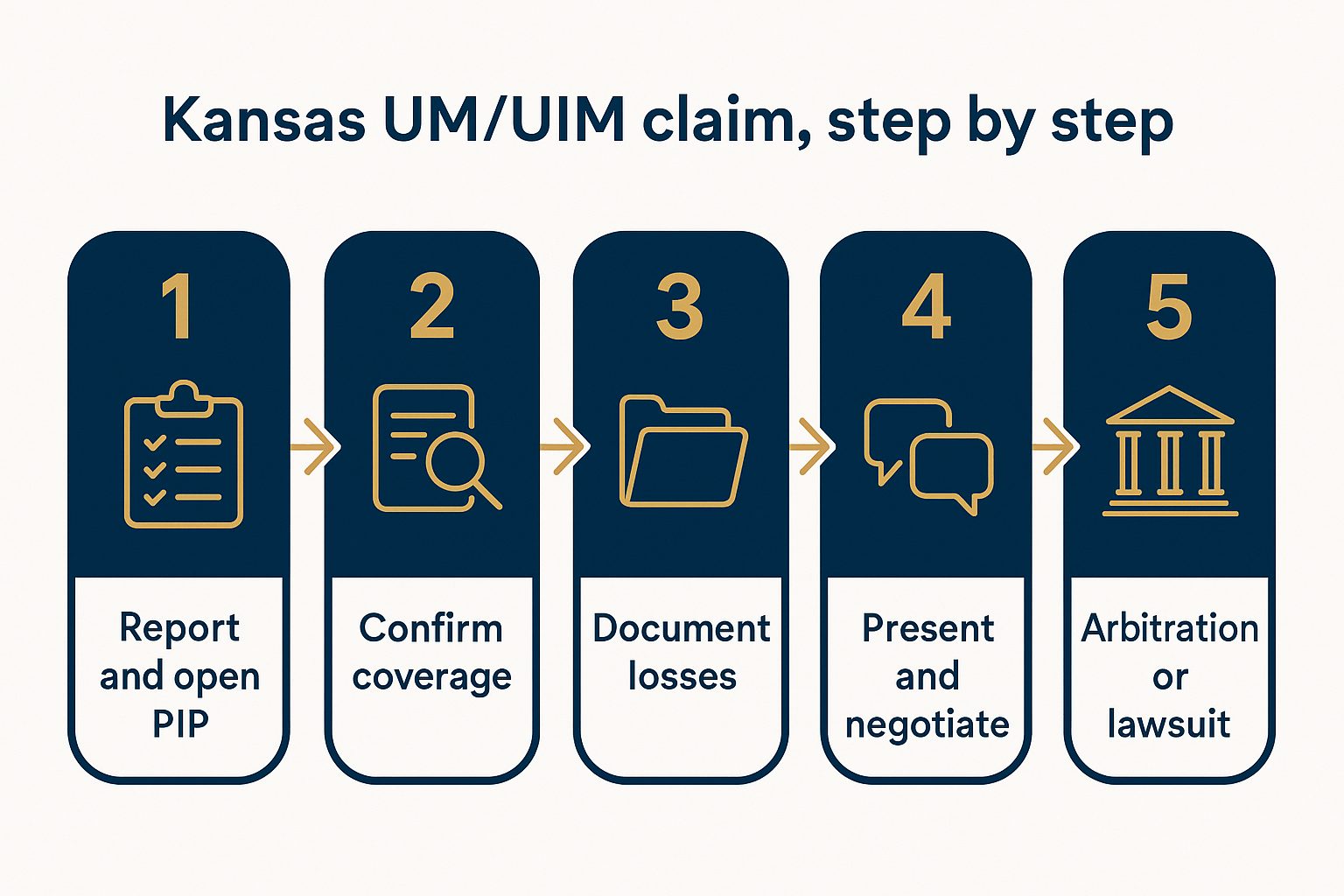

In practice, a Kansas UM/UIM claim usually moves through these stages.

- Report the crash to law enforcement and to your own insurer promptly, and open the PIP claim so your medical bills and wage loss are handled under no-fault while the rest of the claim develops.

- Confirm coverage by reading the policy and declarations page: the UM/UIM limit, the at-fault driver's liability limit (for UIM), and how PIP has paid.

- Document the injuries, treatment, and losses that drive the claim's value.

- Present the claim to your own insurer and negotiate its value, keeping the PIP duplication and any UIM setoff issues in view.

- If the value cannot be resolved, pursue the remedy your policy and Kansas law provide, whether that is arbitration or a lawsuit.

One point is worth understanding up front. In a UM or UIM claim, your own insurer is on the other side of the dispute over how much your claim is worth. They are not adverse to you the way the other driver's insurer is, but they do have a financial interest in valuing the claim conservatively. That is normal, and it is a common reason people want a lawyer involved even when the claim is against their own carrier. For a short plain-English walkthrough of what to expect, the firm's YouTube channel has client-education videos on the injury-claim process.

What are the deadlines for a Kansas UM/UIM claim?

Two clocks matter, and they are not the same.

The first is the statute of limitations on the underlying injury. In Kansas, most personal injury claims must be filed within 2 years under K.S.A. 60-513. This is materially shorter than Missouri's 5-year period, which is one more reason not to carry a Missouri assumption across the state line. The Kansas statute of limitations for personal injury claims, including the discovery rule and other timing wrinkles, is covered in detail on its own page.

The second is the deadline that governs the UM/UIM claim itself. A UM/UIM claim is a claim under your insurance contract, so it is treated as a written-contract claim and generally carries the 5-year written-contract limitations period under K.S.A. 60-511, unless a shorter suit-limitation provision in your policy applies. Because the contract clock and the underlying 2-year injury clock run separately, and because a policy can shorten the time to sue, the deadline that actually controls your claim depends on your policy and your facts.

Separate from any lawsuit deadline, most policies require prompt notice of a UM or UIM claim, and PIP benefits have their own reporting expectations. Because these timelines overlap and the injury deadline in Kansas is short, the safe practice is to treat a UM/UIM claim as time-sensitive and put your insurer on notice early.

How UM/UIM claims play out around Lawrence and Douglas County

Crashes that turn into UM or UIM claims happen on the same roads as any other wreck in Douglas County. The Kansas Turnpike (I-70) at the Lawrence interchanges, the K-10 corridor toward Eudora and Johnson County, Iowa Street and 23rd Street through town, and the two-lane routes out toward Baldwin City and Tonganoxie all see serious collisions. Add student and game-day traffic around KU, and uninsured or underinsured drivers are a real part of the picture. When the at-fault driver in one of these crashes turns out to be uninsured, or flees, the injured driver's own coverage becomes the question.

For drivers in Lawrence, Eudora, Baldwin City, and the surrounding Douglas County communities, that usually means a Kansas policy, Kansas no-fault, and Kansas UM/UIM law, all analyzed together. A civil suit arising from one of these crashes would generally be filed in the District Court of Douglas County. If your situation is a broader car-accident question rather than a coverage question, our Lawrence, KS car accident lawyer page covers the wider process. UM/UIM coverage applies no matter what you were driving, so the same questions come up whether you were in a car, on a motorcycle, or a passenger when an uninsured or underinsured driver hit you.

How Empower Injury Law helps with UM and UIM claims

UM and UIM claims sound simple, your own insurer pays, but in Kansas they turn on details that are easy to get wrong: whether UM or UIM applies, how the limits-to-limits comparison works, how PIP interacts with UIM without paying you twice, the statutory antistacking rule, and short deadlines. We handle these claims for injured drivers and passengers in Lawrence and across Douglas County, and the work usually involves the following.

- Reading your policy and declarations page to confirm the UM/UIM limit you actually carry and how PIP has paid.

- Running the Kansas limits-to-limits analysis to see whether a UIM gap exists at all.

- Coordinating PIP and UIM so the claim is not undervalued and you are not paid twice for the same loss.

- Dealing with your insurer's adjusters and their requests, including recorded-statement requests, so you are not navigating that alone.

- Watching the deadlines, both the 2-year injury clock and any policy notice or suit-limitation provisions.

We work on a contingency fee, which means there is no fee unless there is a recovery, and the initial consultation is free.

Frequently asked questions

Does my own insurance pay if an uninsured driver hits me in Kansas?

Usually, yes, through your uninsured motorist (UM) coverage. UM coverage is part of your own Kansas auto policy and is designed to pay for your bodily injuries when the at-fault driver had no liability insurance or cannot be identified, such as a hit-and-run. You file the claim with your own insurer rather than chasing the uninsured driver directly.

Is uninsured and underinsured motorist coverage required in Kansas?

Yes. Kansas requires uninsured motorist coverage on auto policies, and the underinsured motorist provision is built into it under K.S.A. 40-284, so a Kansas policy generally carries both at the same limit. The commonly stated minimum is $25,000 per person and $50,000 per accident for bodily injury. This differs from Missouri, where underinsured motorist coverage is optional, so the two states should not be analyzed the same way.

What is the difference between uninsured and underinsured motorist coverage?

Uninsured motorist (UM) coverage applies when the at-fault driver had no insurance or cannot be identified, such as a hit-and-run. Underinsured motorist (UIM) coverage applies when the driver had insurance, but the limits were too low. UM is about whether there was any coverage; UIM is about whether the coverage was enough. In Kansas, UIM pays to the extent your own limit exceeds the at-fault driver's liability limit.

Can you stack UM/UIM coverage in Kansas?

Generally no. K.S.A. 40-284 contains an antistacking provision, so the total UM/UIM coverage available for a single claim generally cannot exceed the highest limit of any one applicable policy, regardless of how many vehicles or policies are involved. This is different from Missouri, where stacking turns on policy language and case law.

How does Kansas PIP (no-fault) affect a UM/UIM claim?

Kansas is a no-fault state, so your own PIP coverage pays certain economic losses first, regardless of fault, with statutory minimums set by K.S.A. 40-3103. PIP does not reduce or offset your UM/UIM coverage, but your UM/UIM coverage will not pay again for damages PIP has already covered, so there is no double recovery for the same loss. Missouri has no PIP or no-fault system, so this analysis is specific to Kansas.

How long do I have to file a UM or UIM claim in Kansas?

The underlying injury claim in Kansas generally must be brought within 2 years under K.S.A. 60-513, which is shorter than Missouri's period. A UM/UIM claim is a claim under your insurance contract and is generally treated as a written-contract claim with a 5-year limitations period under K.S.A. 60-511, unless your policy sets a shorter time to sue. Most policies also require prompt notice, so treat these claims as time-sensitive.

What should I do if a hit-and-run driver injured me in Kansas?

Report the crash to law enforcement promptly and notify your own insurer without delay, because your uninsured motorist coverage is generally what responds when the at-fault driver cannot be identified. Prompt reporting does not guarantee coverage, but a delayed or missing report can give the insurer an argument to contest the claim.

Talk with a Lawrence UM/UIM lawyer

If an uninsured or underinsured driver injured you in Lawrence or elsewhere in Douglas County, you can talk through your options with Empower Injury Law at no cost. We will look at your policy, run the Kansas coverage analysis, and tell you honestly what we think the claim involves. There is no pressure and no fee unless there is a recovery.

Call the Lawrence office at 785-367-6937, email [email protected], or request a free case review through the form on this page. Our Lawrence office is at 831 Massachusetts St, Lawrence, KS 66044, and we serve clients in Lawrence, Eudora, Baldwin City, Tonganoxie, and the surrounding Douglas County communities.